- What We Drive

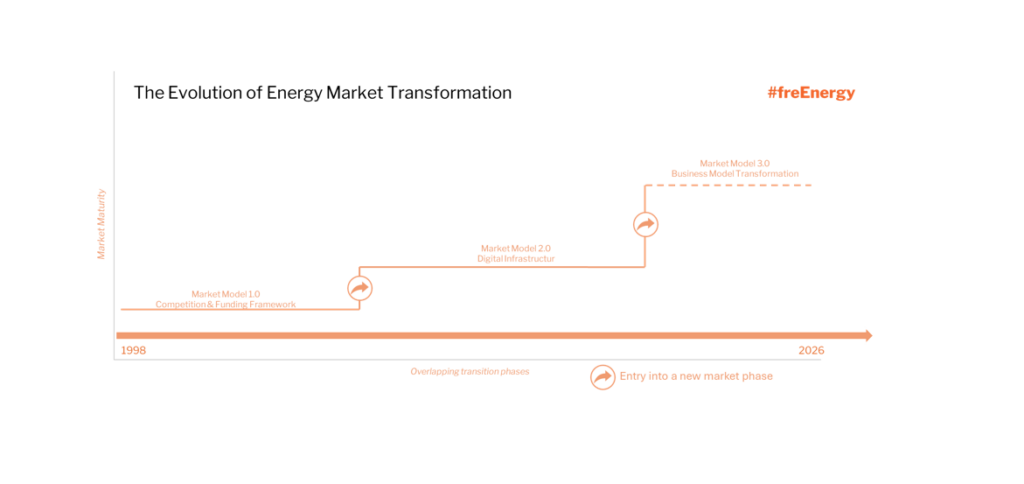

Trilogy of Energy Market Transformation

Market Model 3.0 – A Call for Discussion

Thirty years of energy system transformation leave their mark. Marks in the form of laws that reordered markets, IT systems that had to be adapted, business models that emerged and disappeared again, that changed. Organizations were forced to keep pace, driven by regulation.

This article is the beginning of an attempt to identify patterns from these three decades. Not as a scientific analysis, but as a reflection on selected milestones. A look back – to look forward. Whoever recognizes early on where the market is heading can prepare and build the necessary capabilities in time – in the business departments, in IT, in products. It is not about predicting every detail. The concrete form will take shape along the way. It is about pattern recognition. Patterns we need to anticipate the future Market Model 3.0 – and to prepare processes, IT and organizations accordingly.

In this sense, this article is above all one thing: an invitation to discuss.

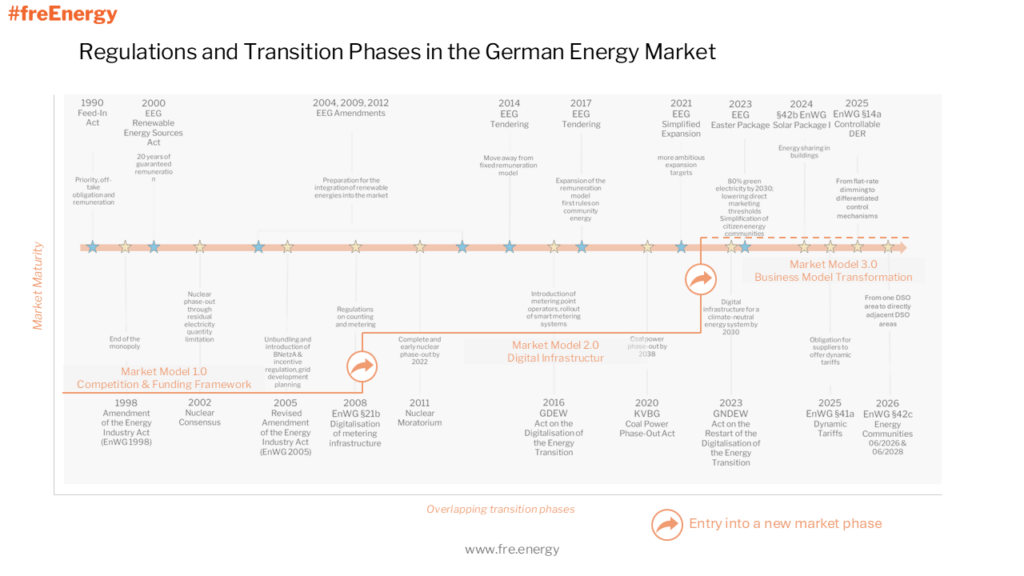

The chart shows an extract of the regulatory frameworks that have shaped the German energy market from 1990 to the present and driven the transformation of the energy market model. A complex system has emerged, containing countless interdependencies, an understanding of which is essential for future planning.

Looking at the timeline, three phases can be broadly identified. Let us call them Market Model 1.0, 2.0 and 3.0. The boundaries between the phases are deliberately drawn roughly – in reality they overlap. Each phase was initiated by a legislative impulse, then shaped further by regulation and market development. And the optimization continues to progress in many areas to this day.

The focus of this analysis is on the German market, in order to remain as concrete as possible – but the patterns are similar across Europe. This is because most national regulatory frameworks involve the transposition of EU law. Analogies can also be found globally, as the expansion of renewables is progressing worldwide and with it the necessity of their market-oriented integration. In the following, we take a brief look at each of the three phases.

Market Model 1.0 – Competition, Unbundling and Regulatory Framework

The 1998 amendment to the Energy Industry Act (EnWG) ended the vertically integrated territorial monopoly; the Federal Network Agency (BNetzA, 2005) enforced non-discriminatory network access and regulatory unbundling, after the negotiated Third-Party Access (TPA) model had failed. In parallel, the Renewable Energy Sources Act (EEG) of 2000 created the investment framework for the ramp-up of renewables through feed-in priority and guaranteed remuneration – successive amendments up to 2014 completed the transition from a fixed-price to a tendering model. Market Model 1.0 thus provided the regulatory and subsidy framework on which the subsequent structural transformation could build.

Market Model 2.0 – Digital Infrastructure: Data, Metering and Processes

The legal framework was in place – but the physical energy system and its IT infrastructure remained largely at the level of a centralized supply model. Millions of meters were read once a year, supplier changes took too long, and the data basis for intelligent grid management was lacking. Legislation addressed this gap in 2008 with EnWG §21b: the creation of a digital infrastructure layer without which the market-based integration of renewable energies is technically impossible. The 2016 Act on the Digitalization of the Energy Transition was the follow-up regulation: the metering point operator was established as an independent market role, mandatory installation obligations for smart metering systems were set out in stages according to consumption and generation capacity, and the BSI was mandated as the certification authority for smart meter gateways. Existing processes were adapted and IT systems upgraded accordingly.

In a European comparison, Germany today lags significantly behind with a smart meter coverage rate of just 5.5% (as of 27 March 2026). The GNDEW of 2023 targets full coverage by 2030 – without this interface between grid and market, the energy transition will remain structurally incomplete and will impede the transformation of the energy system.

Market Model 3.0 – Flexibility and Business Model Transformation

The growing share of variable renewables – combined with the electrification of the mobility and heating sectors, as well as the structurally growing energy demand from AI data centers – makes flexibility the central system resource.

§14a EnWG regulates DER (Decentralized Energy Ressources) as active grid components. Dynamic tariffs and time-variable grid charges set consumer incentives. The overhaul of the state subsidy logic will fuel direct marketing and energy sharing models. The market will be fundamentally transformed, business models rethought. The task is to fully integrate renewables into the market and optimally orchestrate the sectors. To achieve this economically, system services must be provided at scale. A new quality of digital collaboration is required – in real time, across system boundaries and market roles.

Experience teaches us: laws work – rarely at the first attempt, revisions are part of the pattern. Market Models 1.0 and 2.0 followed the logic: laws initiate, regulation drives forward, the market develops further – successful companies ultimately make economically viable what was previously only an obligation.

What distinguishes Market Model 3.0 from its predecessors is:

- Renewable energies have a business case for many customers – even without state subsidies. Rising costs for oil and gas are increasing the attractiveness of electrification and mobilizing additional capital.

- Regulation is increasing the pressure to roll out smart metering infrastructure, which is essential for the development of innovative business models.

- Legislation has created a framework for new business models. Energy sharing, for example, reaches target groups that have so far been left behind by the energy transition.

- Not only classic energy suppliers are in search of scalable business models. Sectors are converging.

- Internationally, markets such as the UK (V2G), the Nordics (dynamic tariffs & load management), Australia (VPP and P2P) and Austria (energy communities) demonstrate that new business models are scaling successfully.

These five characteristics have the potential to unleash a momentum that goes far beyond the regulatory push – it gets to the heart of the matter, to the business models themselves. To the question of how the business case for using renewable energy looks from the customer’s perspective. The full-supply model for customers with electrical energy has been declining for years. Today it is increasingly important to secure the residual supply and to tap new revenue streams – ideally through subscription models. What has long been anticipated is now happening: existing models are being transformed at increasing speed. New market players and platform solutions are entering the market, and traditional roles as well as collaboration models are being rethought.

In this phase: those who get hands-on and act while keeping an eye on the cost-benefit ratio are at an advantage – practice beats theory. The search for target-group-specific models that scale has begun. According to a recent study by Boston Consulting Group, households with a heat pump, battery storage and electric vehicle can already save between €350 and €450 per year (or 20–30%) through dynamic tariff optimization alone – with advanced market integration, this figure could increase two to threefold. Such prospects will quickly drive demand – and thus create pressure to develop suitable offerings.

Whoever succeeds in making energy more cost-effective for their customers will be successful. The foundations are in place. Which business strategies will prevail and what the appropriate IT and process architectures will look like – these will be the exciting questions that need to be answered.